Employer Misclassified Employee as Independent Contractor. I did not realize it when I accepted the job. I realized it when something small stopped making sense. Everyone around me talked about payroll, tax withholding, benefits enrollment, overtime rules, and year-end forms like those were normal parts of the job. Mine never looked the same. My pay came in, but it never felt like employee pay. Then the real problem showed up: no withholding, no benefits access, no normal payroll record, and eventually a tax form that told me the company had been treating me like an independent contractor the whole time.

That is usually how Employer Misclassified Employee as Independent Contractor situations start. Not with a dramatic meeting. Not with a written warning. It starts when the worker notices that the company expects employee-level control over the job, but the payroll and tax setup looks like a contractor arrangement. That mismatch is where the real risk begins, because once the wrong classification enters the system, it can affect taxes, overtime, benefits, unemployment eligibility, and internal payroll routing all at once.

Employer Misclassified Employee as Independent Contractor problems do not always come from one obvious decision. Sometimes HR entered the wrong status during onboarding. Sometimes the company intentionally used contractor classification to reduce cost. Sometimes a worker was brought in quickly, put on a contractor code, and then left there even after the role became identical to a normal employee position. Whatever the reason, the worker is usually the one left with the financial damage.

If this is happening to you, the most important thing to understand is simple: the label the company used is not the only thing that matters. The actual working relationship matters. If the company controls your hours, directs your daily work, integrates you into the business like a regular employee, and treats you like staff in every practical way except payroll classification, then this is no longer a minor paperwork issue. It is a structural employment problem.

Before you go further, it helps to understand how pay and status issues usually get created inside company systems.

How this problem usually first shows up

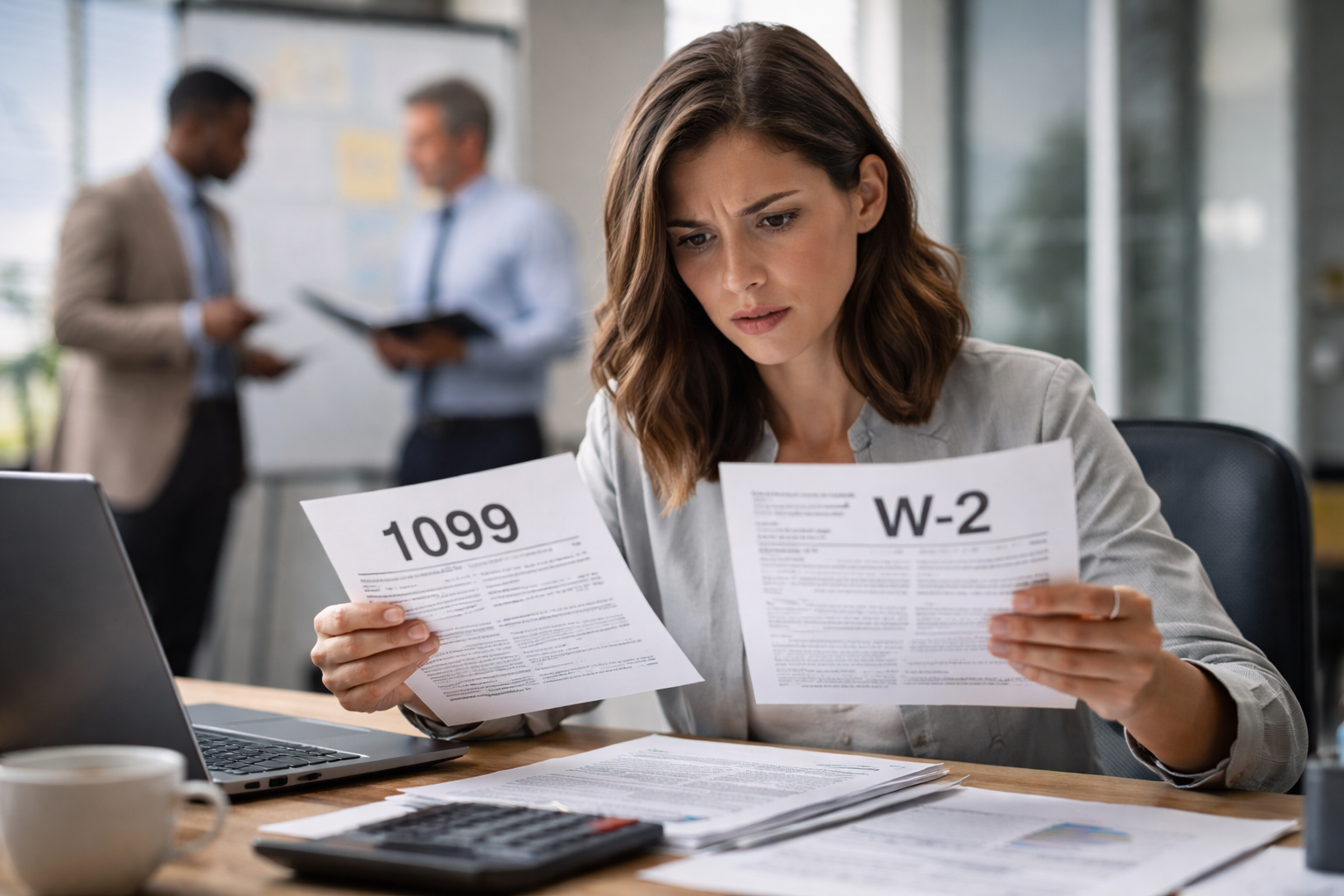

Employer Misclassified Employee as Independent Contractor often becomes visible through side effects, not through a direct admission. Most workers do not get an email saying they were misclassified. They discover it because something else feels wrong.

- Your pay has no tax withholding even though your schedule is tightly controlled

- You are told when to work, how to work, and who to report to, but payroll says you are not an employee

- You are excluded from benefits enrollment while doing the same kind of work as employees

- You work overtime, but there is no overtime pay calculation

- You receive a 1099 even though the role functioned like a normal job

- You are told to follow internal company policies like staff, but are paid like an outside vendor

Employer Misclassified Employee as Independent Contractor cases usually feel confusing at first because the company relationship looks like employment in practice, while the pay structure looks like contract work on paper. That gap between operational control and payroll treatment is the detail that usually matters most.

Why companies do this

There are several reasons an Employer Misclassified Employee as Independent Contractor situation happens. Some are administrative. Some are deliberate. Some start as temporary shortcuts and later become permanent problems.

From the company side, contractor classification can reduce labor cost. The company may avoid employer-side payroll taxes, overtime exposure, unemployment insurance contributions, benefit costs, and certain administrative burdens. That does not automatically make every contractor relationship improper, but it does explain why some businesses push borderline roles into contractor status.

Inside payroll and HR systems, classification decisions are often set very early. A worker profile may be created under a contractor code, sent into a vendor payment workflow, and then connected to tax reporting rules that never resemble employee payroll. Once that happens, every downstream system follows the same logic. If the initial status is wrong, the tax engine, pay engine, benefits module, and reporting layer may all continue processing the worker incorrectly.

Employer Misclassified Employee as Independent Contractor issues also appear in fast-moving environments. Startups, remote teams, seasonal operations, short-staffed offices, and outsourced payroll setups are especially prone to this because onboarding gets rushed and classification review is weak.

What the company may be seeing internally

One reason workers struggle to fix Employer Misclassified Employee as Independent Contractor cases is that the company may not be looking at the same problem the worker is looking at. The worker sees unfair treatment. Payroll may only see a status code. HR may only see the original onboarding choice. Finance may only see a lower-cost payment structure already built into the system.

That matters because when you raise the issue, the first answer may be misleadingly simple: “That is how you were set up.” But that does not resolve anything. It only tells you where the problem lives.

If payroll says one of the following, the classification issue may already be embedded in multiple systems:

- “You are not showing as an employee in payroll.”

- “You were set up as a contractor when you started.”

- “Benefits are not available under your status.”

- “Tax withholding was not configured for your profile.”

- “You are paid through accounts payable, not employee payroll.”

Those are not just excuses. They are clues about where the misclassification sits inside the company’s records.

Employer Misclassified Employee as Independent Contractor cases are often easier to understand when you stop thinking only in legal terms and start thinking in system terms too. The company may have built your status into payroll, tax, and benefits logic from the start.

Self-check: does your job actually look like employee work

If you are trying to figure out whether Employer Misclassified Employee as Independent Contractor applies to your situation, start with direct comparison. Do not focus only on what the contract said. Focus on how the job actually operated week to week.

Check your situation against these points:

- Did the company set your work hours?

- Did a manager supervise your daily tasks?

- Did the company require internal meetings, rules, or reporting procedures?

- Did you use company systems, software, or equipment as part of normal work?

- Was your role central to the company’s regular operations?

- Could you realistically do the work your own way, or were you expected to follow company process like staff?

If most of these are true, the working relationship may look much more like employment than independent contracting.

Employer Misclassified Employee as Independent Contractor becomes much more serious when the company controls not just the final result, but the method, schedule, supervision, and structure of the work.

Where workers usually get hurt first

Employer Misclassified Employee as Independent Contractor does not create only one kind of damage. It usually creates several at once.

- Unexpected self-employment tax exposure

- No overtime even after long workweeks

- No access to health, retirement, or leave-related benefits

- No normal paycheck withholding structure

- Problems with unemployment claims later

- Confusion about year-end tax reporting

The financial harm often appears late. That is one reason this situation feels so destabilizing. A worker may continue doing the job for months, assuming the company has the setup right, only to discover later that the entire payment structure was shifted away from employee protections.

The danger is not only what you lost on each paycheck. The danger is that the company may have built the loss into every pay cycle from the beginning.

Different versions of the problem

Employer Misclassified Employee as Independent Contractor does not look the same in every workplace. Your next step depends on which version you are dealing with.

If you were hired quickly and never properly onboarded:

This may be an HR and payroll setup failure. Ask what worker type, tax profile, and pay channel your account was assigned at onboarding.

If you used to be an employee and were shifted into contractor treatment:

This may indicate a compensation restructuring issue. Compare what changed: taxes, overtime, benefits, reporting lines, and written role expectations.

If the company calls everyone in your role a contractor:

This may be a broader classification model, not an isolated error. Your case may depend heavily on how much control the company exercises over the role.

If your job title says contractor but daily reality looks like staff employment:

Document the gap between the written label and actual work control. That gap is often the strongest part of the worker’s position.

Employer Misclassified Employee as Independent Contractor problems should not be approached with a one-size-fits-all script. The stronger move is to identify which structure produced the problem and then gather proof around that structure.

What to document before you complain

If you raise an Employer Misclassified Employee as Independent Contractor issue without preparation, the company may reduce it to a disagreement about paperwork. That is why documentation matters.

- Offer letters, contracts, and onboarding emails

- Schedules assigned by managers

- Messages directing how work must be done

- Records of required meetings, policies, and supervision

- Time records showing long hours or overtime-style work

- Pay statements, invoices, tax forms, and missing withholding evidence

Document first. Argue second. The more clearly you can show company control over your work, the harder it becomes to treat the issue like a misunderstanding.

If the company has also mishandled your pay flow, this guide may help you identify overlapping payroll damage.

What not to do

Employer Misclassified Employee as Independent Contractor situations often get worse because workers make avoidable mistakes in the first response phase.

- Do not assume the company’s label settles the issue

- Do not ignore the problem until several tax years pass

- Do not rely only on verbal explanations from payroll

- Do not throw away work records that show daily control

- Do not reduce the issue to “I want benefits” when the real issue is classification structure

One of the biggest mistakes is accepting the company’s framing. If the employer responds by saying, “That is just how contractors are paid,” that does not answer whether contractor classification was appropriate in the first place.

You are not only checking how you were paid. You are checking whether you were placed into the wrong category to begin with.

What to do right now

If you believe Employer Misclassified Employee as Independent Contractor applies to you, take these steps in order.

- Confirm what status code or worker type the company assigned you

- Collect records showing the level of company control over your work

- Compare your daily role with employee roles doing similar work

- Identify every pay-related consequence: withholding, overtime, benefits, tax form, unemployment risk

- Ask HR or payroll for a written explanation of your classification

This is where many workers finally get clarity. Once HR or payroll has to explain the classification in writing, the issue often becomes more concrete.

Employer Misclassified Employee as Independent Contractor should be handled as a full-status problem, not only a paycheck problem. That means looking at every connected area the classification changed.

If you want to understand how federal agencies evaluate worker classification disputes, the official guidance from the IRS explains the control and relationship factors used to determine whether a worker should be treated as an employee or independent contractor.

Official reference:

IRS Worker Classification Guidance

Recommended Reading

If your classification problem overlaps with payroll setup or status coding, read this next to compare how worker status errors show up inside employment systems.

Key Takeaways

- Employer Misclassified Employee as Independent Contractor is different from a simple payroll typo.

- The biggest issue is usually the gap between how the job operated and how the worker was classified.

- Misclassification can affect taxes, overtime, benefits, and unemployment-related protections at the same time.

- Payroll, HR, and tax systems may all be following one wrong worker-status code.

- Workers should document control, schedule, supervision, and company integration before escalating the issue.

- The company’s label is important, but the real working relationship is often more important.

FAQ

What is the main issue in an Employer Misclassified Employee as Independent Contractor situation?

The main issue is that the company may be treating a worker like an employee in daily operations while paying and reporting that worker like a contractor.

How do workers usually discover this problem?

Most workers discover it through missing withholding, missing benefits, missing overtime, or a year-end tax form that does not match how the job actually worked.

Does this only affect taxes?

No. It can also affect overtime treatment, benefits access, unemployment-related protection, and how the worker is handled in payroll systems.

What is the first practical step?

Find out exactly how the company coded your status in payroll or HR, then gather records showing how much control the company had over your work.

Is this the same as a simple employee status typo?

Not always. A typo may be a setup error. Employer Misclassified Employee as Independent Contractor often involves a broader mismatch between actual job reality and the category used by the company.